Commercial Real Estate Jargon Explained

by Erbe Wealth · Published · Updated

Commercial real estate seems to be intimidating to a lot of people, especially when they receive a property summary of a new offering that we have. There are lots of words in that offering that the novice investor in commercial real estate probably doesn’t understand, and that can be a bit intimidating.

I want to break down some of these terms because once you understand them, it isn’t as complicated as people think.

Multifamily Real Estate

The first is multifamily real estate, which is a type of commercial real estate. Often people ask, “What does that mean exactly?” Basically, multifamily means apartment complexes. Technically, it is considered a multifamily commercial property if there are five units or more. As for investing with us though, we typically have properties with 50 to 500 units.

There are actually many types of commercial real estate, including office buildings, medical centers, shopping centers like retail, warehouses, hotels, and even land. Our specialization is in multifamily real estate.

Capital Expenditures

Another term that people haven’t heard of is the term cap ex. Cap ex is short for capital expenditures, and it is the money that is set aside and used for improvements and necessary costs.

We try to find properties that may look a little run down and probably just haven’t had the TLC of a good owner. Those properties have some things that really are not taken care of on a regular basis. In our budget and our underwriting, we always include a percentage of income that we distribute to improve the property. Cap Ex is not repairing something that has broken, but rather it is actually improving something. It is important to improve the appearance of the property.

Net Operating Income

Another term that people are not familiar with is net operating income. Our apartment complex is a business, and there are expenses that go out. For instance, there are expenses like property managers and doing repairs. However, we also have income coming in, like rent or different fees. The income minus the expenses equal the net operating income. As the professionals running this property, we want to increase and improve the NOI. The higher the net operating income is, the higher the value of the property is, and so that is our number one goal of what we’re trying to achieve.

Loan to Value Ratio

Another term that people see is loan to value ratio (LTV).

The LTV is short for loan to value ratio, which is used in commercial mortgage and multifamily property financing to determine the ratio of a particular debt. Many investors think that we raise all of the money to purchase the apartment community from our investors, and that’s not the case. We get a loan on the property.

Loan to value can be thought of as the amount of leverage in a transaction. The higher the leverage, the higher the risk for both the lender and the borrower, but particularly for the lender. Borrowers typically aim for higher loan to value ratios as it means they will need to bring less cash to the table and can maximize the potential profits for their investors. The formula for LTV is total loan amount divided by estimated property value.

For example, a $750,000 loan on a property worth one million would be 75% loan to value. Loan to value is perhaps the most important measure of risk that lenders use when determining how much funding they will provide for a specific property and loan to value limits vary greatly between lenders. In general, 75 to 80 percent is what we aim to get on our multifamily properties.

Repositioning

Another unfamiliar term that people see in our documents is repositioning and that can mean a lot of different things, but here’s how we use it: we complete micro renovations on our newly acquired properties and repositioning means that we are doing some kind of construction. It’s the work and somewhat heavy lifting to reposition this property as a nicer one.

Reposition is what we strive to do for every property we have. Some syndicators completely gut the units and do full renovations, but that’s not something we do in any of our properties. We’re very comfortable with a micro renovation. This is where we replace the flooring, paint, and put in lighting fixtures. We update the kitchen with the appliances and update the bathrooms. It’s a very light renovation, but makes everything nicer, so that is what repositioning means for us.

Sponsor

A sponsor is the person or team that puts together a syndication. They are the ones that find the deal, bring it to people, and run the deal. I encourage you to check my article about the different phases of a syndication to kind of get an idea of what an average sponsor should do. https://erbewealth.com/education/3-phases-of-a-real-estate-syndication/

Cash on Cash Return

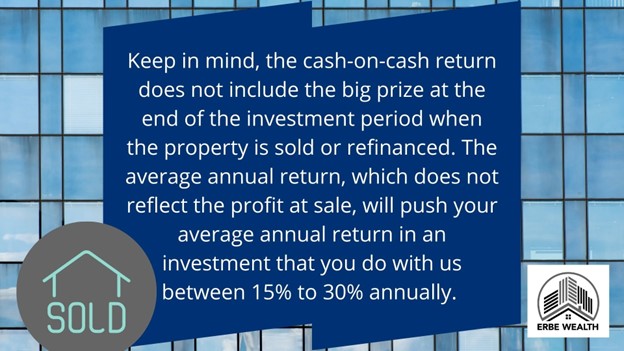

Another unknown term is cash on cash return. It is a measure of the return on your investment. It is calculated on an annual basis by simply taking the cash flow you receive and dividing it by your initial investment. So, for example, if an investor participates in a syndication by putting a typical investment amount of $100,000 into the deal. The investor receives $8,000 in distributions during the first year. So, 8,000 divided by a 100,000 equals 8% cash on cash return. It’s typical in our multi-family opportunities to get an annual, cash on cash return of between 6% to 9% percent. The cash-on-cash returns should increase the longer the property is held. Over the life of the investment, the cash-on-cash return should be going up each year as the sponsor is implementing the business plan to optimize the property.

Keep in mind, the cash-on-cash return does not include the big prize at the end of the investment period when the property is sold or refinanced. The average annual return, which does not reflect the profit at sale, will push your average annual return in an investment that you do with us between 15% to 30% annually.

Building Classification

The last term we will look at is building classification. In multifamily real estate, you hear a lot about type A properties, B properties, and C properties. What are they and does it matter which one you choose to invest in?

A class properties are the nicest brand-new properties that you often see in your downtown area. They have a gym, a bar, lots of amenities almost to where it is almost like staying in a hotel. We don’t invest in A class property because think of it as sort of buying a new car. There really is no way to increase the value of that property other than maybe the natural appreciation that would occur if it’s in a really great area. Our group is always looking to buy value add properties, which means we put value in by updating the property and making it worth more than when we got it to begin with.

We buy B class properties which is the next class down, but we look for these in great areas. These properties have, you know, working professionals in them. They are located in really good school districts and stable, safe areas.

We like these because historically B properties have performed fantastic through recessions. If there’s a recession, the A-Class tenants want to downsize and save money, and homeowners might not be able to afford their houses. Yet they have a family and they still want to be in a good, safe area with good schools. Being in a B class property makes sense and that is actually historically what we’ve seen through past recessions.

The C class properties are the oldest. They have low rents. They need updating and they are usually not is a great area. It usually has people that are not paying the rent on time.

We do not buy any C class assets.